On the Market

Property Type: Farmland Price: $10,500,000 Location: Nevada [...]

Property Type: Farmland Price: $19,816,000 Location: Montana [...]

Property Type: Estate Price: $10,188,750 Location: Arkansas [...]

Property Type: Farmland Price: $19,816,000 Location: Montana [...]

Property Type: Estate Price: $10,188,750 Location: Arkansas [...]

Property Type: Ranchland Price: $8,900,000 Location: California [...]

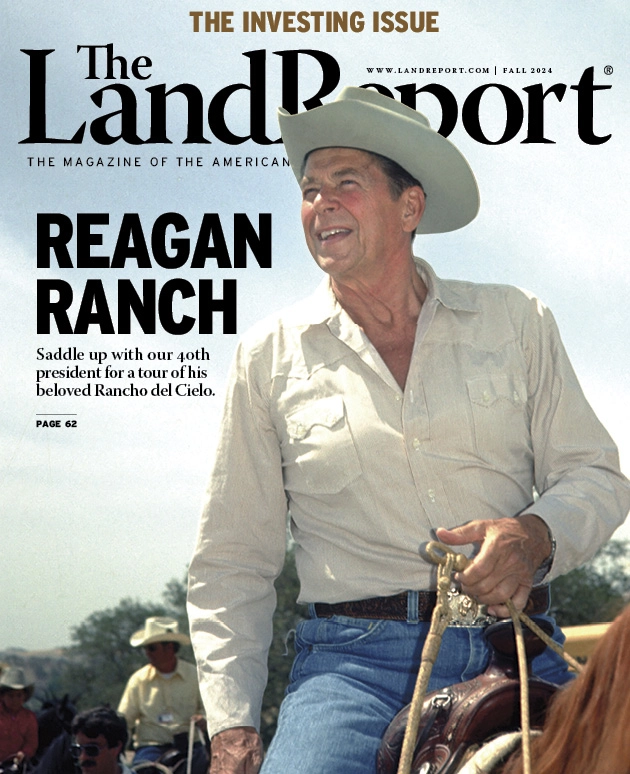

Landowner Spotlight

Texas’s largest largest landowners are historic, right? That’s a given. [...]

The Magazine Of The American Landowner

Please sign me up to receive breaking news and updates from The Land Report:

more popular stories

The April edition of the Newsletter of the American Landowner [...]